How to Read Your Credit Report

Confused by how to read your credit report? This step-by-step guide explains every section of your Equifax, Experian, and TransUnion reports in plain English — including what to dispute.

5/25/202610 min read

How to Read Your Credit Report Step by Step

By A Paralegal's Guide to Credit Repair | paralegalguides.com

Can I tell you something that surprises almost everyone who hears it?

The majority of people who are actively worried about their credit — who lie awake thinking about their score, who get declined for loans, who pay higher interest rates because of their history — have never actually sat down and read their credit report.

Not really read it. Not line by line, section by section, with a clear understanding of what they're looking at and why it matters.

And honestly? That's not their fault. Credit reports are not designed to be user-friendly. They're dense, formatted oddly, full of industry codes and abbreviations, and organized in a way that makes sense to a lender but feels like a foreign language to everyone else.

But here's the thing: you cannot fix what you don't understand. Every dispute letter, every goodwill letter, every pay-for-delete negotiation we've covered in this series starts in the same place — with you pulling your credit report and knowing exactly what you're looking at.

So that's what this post is about. A plain-English, section-by-section walkthrough of your credit report — what's in it, what it means, what to look for, and what to do when something doesn't look right.

By the time you finish reading this, your credit report will never feel intimidating again.

Let's go.

Step 1: Get Your Credit Reports (All Three of Them)

Before we can talk about how to read your credit report, you need to actually have it in front of you.

Here's what most people don't realize: you have three credit reports, not one. Equifax, Experian, and TransUnion each maintain their own separate file on you. While they often contain similar information, they are not identical. A creditor might report to all three bureaus, or just one or two. An error might appear on one report and not the others. A collection account might show different balances across bureaus.

This is exactly why reviewing all three matters — and why disputing an item with one bureau doesn't automatically fix it on the other two.

Where to get them for free:

The official, federally mandated source for free credit reports is AnnualCreditReport.com. Under federal law, you're entitled to one free report from each bureau every 12 months. In recent years, all three bureaus have also offered free weekly access through that same site, which is genuinely useful when you're actively working through a dispute process and want to monitor changes.

What you'll need to verify your identity:

Your Social Security number

Your date of birth

Your current and recent past addresses

Possibly answers to identity verification questions based on your credit history

Once you have all three reports pulled — whether as PDFs, printed pages, or accessed online — you're ready to start reading.

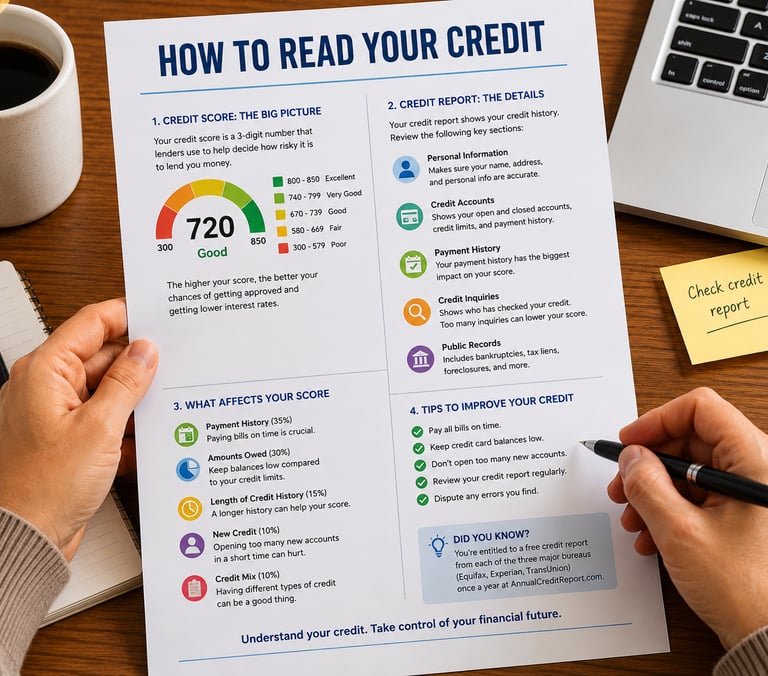

Step 2: Understand the Five Sections of Your Credit Report

Every credit report, regardless of which bureau produced it, is organized into five main sections. The formatting and terminology may vary slightly between Equifax, Experian, and TransUnion, but the underlying structure is consistent. Here's what each section contains and what to look for.

Section 1: Personal Information

This section contains the identifying information the bureau has on file for you:

Your full name (and any name variations they've recorded)

Your current and previous addresses

Your date of birth

Your Social Security number (usually partially masked)

Your current and previous employers

What to look for:

Errors in your personal information are more common than you'd think — and more important than most people realize. An incorrect address might seem harmless, but it can be a sign that someone else's accounts have been mixed into your file (a problem called a "mixed file," which is more common with similar names). An unfamiliar address could indicate identity theft or an account you didn't open.

Check that your name is spelled correctly, your SSN matches (to the extent you can verify the masked digits), and that you recognize every address listed. If something doesn't match, flag it.

Important note: You cannot dispute accurate personal information simply because you don't want it there. But you can dispute information that is genuinely incorrect.

Section 2: Account Information (Also Called "Trade Lines")

This is the longest and most important section of your credit report. It lists every credit account you have — or have had — including:

Credit cards (open and closed)

Mortgages

Auto loans

Student loans

Personal loans

Retail store cards

Lines of credit

For each account, the report will typically show:

Account name and number (usually partially masked)

Account type (revolving, installment, mortgage, etc.)

Date opened

Credit limit or original loan amount

Current balance

Payment status (current, 30 days late, 60 days late, 90 days late, charged off, etc.)

Payment history — often shown as a month-by-month grid going back several years

Date of last activity

Date the account is scheduled to age off your report

What to look for:

This section is where most credit report errors live, and where most of your dispute work will happen. Go through every account carefully and ask yourself:

Do I recognize this account? If not, it may be identity theft or a mixed file.

Is the balance correct?

Is the credit limit accurate? (An incorrectly low limit can hurt your credit utilization ratio)

Does the payment history match my records? Look for late payments that you have documentation showing were made on time.

Is the account status correct? A "charged off" account you paid in full should reflect that payment.

Is the date opened correct? An incorrect open date can affect how long the account ages off.

Is the "scheduled removal date" accurate? Most negative items must be removed after seven years from the date of first delinquency. If an item is scheduled to remain longer than that, it may be worth flagging.

Go through this section slowly. It is worth the time.

Section 3: Collections

If any of your accounts were sent to a collections agency, they will appear here — separate from the original account listing. You may see both the original account in Section 2 (marked as charged off or transferred) AND the collection account in Section 3. This is normal, though it can feel like you're being penalized twice for the same debt.

Each collection entry will show:

The name of the collection agency

The original creditor's name

The account number (usually masked)

The date the account was placed in collections

The balance being claimed

The date of first delinquency (this is the date that starts the seven-year clock)

What to look for:

Does the collection account belong to you? If not, dispute it immediately.

Is the date of first delinquency accurate? This date is critical — it determines when the account must be removed from your report. A collector cannot reset this date to extend how long the item appears.

Is the same debt listed more than once? This happens when debt is sold from one collector to another. Only the current collector should appear; duplicates should be disputed.

Has the account already passed the seven-year mark? If so, it should no longer appear and you can dispute its presence.

Is the balance accurate? Inflated balances in collection accounts are not uncommon.

Section 4: Public Records

This section contains information from court records, including:

Bankruptcies (Chapter 7 and Chapter 13)

Civil judgments (in some states and situations)

Tax liens (though these have been largely removed from credit reports in recent years following a rule change)

What to look for:

Bankruptcies are the most common item in this section. A Chapter 7 bankruptcy stays on your report for ten years from the filing date. A Chapter 13 bankruptcy stays for seven years. If a bankruptcy appears here, verify that the filing date, type, and discharge status are accurate.

If a public record appears that you don't recognize, or that you believe has been removed through legal proceedings, dispute it with supporting documentation from the court.

Section 5: Inquiries

Every time someone accesses your credit report, it creates an inquiry. This section lists them all — but not all inquiries are created equal.

Hard inquiries occur when you apply for credit — a credit card, a mortgage, an auto loan. Hard inquiries can slightly lower your credit score and remain on your report for two years. Multiple hard inquiries in a short window (especially for mortgage or auto loan shopping) are often treated as a single inquiry by scoring models.

Soft inquiries occur when you check your own credit, when a creditor does a routine review of your existing account, or when a company checks your credit for a pre-approval offer. Soft inquiries do NOT affect your credit score and are generally only visible to you — not to lenders.

What to look for:

Hard inquiries you don't recognize. An unfamiliar hard inquiry could indicate that someone is attempting to open credit in your name without your knowledge. If you see one you didn't authorize, dispute it and consider placing a fraud alert or credit freeze.

Old hard inquiries. After two years, hard inquiries should no longer appear. If they do, dispute them.

Step 3: Use a Checklist — Don't Wing It

Reading your credit report without a systematic checklist is like trying to proofread a document by skimming it. You will miss things. Errors are easy to overlook when you're reviewing dozens of accounts, especially if you're not sure exactly what you're looking for.

A good credit report review checklist walks you through every section, every field, and every question you need to ask — account by account, bureau by bureau. It keeps you organized, ensures you don't miss anything, and gives you a reference point when you start writing dispute letters.

The A Paralegal's Guide to Credit Repair toolkit includes a complete credit report review checklist designed specifically for this purpose — one that mirrors the structure above and prompts you to look for every common category of error. More on that at the end of this post.

Step 4: Know the Most Common Credit Report Errors

Knowing what to look for in theory is one thing. Knowing the specific errors that appear most often — based on real consumer experience — is another. Here are the ones that show up again and again.

Accounts that don't belong to you. This can happen due to identity theft, a mixed file (your information confused with someone who has a similar name or SSN), or data entry errors at the creditor level. Any account you don't recognize should be investigated immediately.

Incorrect payment status. An account reported as 60 days late when you have a bank statement showing the payment cleared on time. This is one of the most common — and most disputable — errors.

Wrong balance or credit limit. A credit card with a $5,000 limit reported as $2,500 artificially inflates your utilization ratio and hurts your score. Always verify limits and balances.

Duplicate accounts. The same debt listed twice — often when it's been sold from one collector to another, and both appear on your report simultaneously.

Outdated negative information. A charge-off from eight years ago that should have aged off but hasn't. Or a collection account where the date of first delinquency has been inaccurately reset to extend its life on your report.

Incorrect account status. A closed account reported as open (or vice versa). An account included in bankruptcy that still shows a balance due.

Mixed files. If your name is common, or if a data entry error was made somewhere along the way, someone else's accounts can end up in your file. This can look like a collection account, a bankruptcy, or a string of late payments — none of which are yours.

Step 5: Document Everything Before You Dispute

Before you write a single dispute letter, do this: document every error you find in writing.

Create a list — or use a dispute tracker — that includes:

The bureau reporting the error (Equifax, Experian, and/or TransUnion)

The account name and number

The specific error (what is wrong, and what it should say)

Any supporting documentation you have (payment records, statements, court documents)

The date you identified the error

This documentation is your roadmap. It tells you exactly what letters to write, to whom, about what — and it ensures that when you send those letters, they are specific, organized, and backed by evidence.

Vague disputes ("this account is wrong") are far less effective than specific ones ("this account shows a 30-day late payment in March 2023; enclosed is a bank statement showing the payment cleared on March 3rd, 2023, within the billing cycle"). Specificity is your leverage.

Step 6: Know What Happens Next

Once you've read your reports, identified errors, and documented everything, you're ready for the next phase — writing and sending dispute letters.

We covered the full spectrum of credit repair letters in Article #3 of this series, including credit bureau dispute letters, follow-up letters, method of verification requests, and more. If you haven't read that yet, it's a natural next step from here.

The short version of what comes next:

Send credit bureau dispute letters for inaccurate or unverifiable items

Send goodwill letters to creditors for accurate late payments (Article #2)

Send debt validation letters to collectors before paying anything (Article #1)

Track every letter, every response, every deadline

The credit repair process is not complicated. It is detailed. There's a difference. Complicated means it requires special expertise you don't have. Detailed means it requires careful attention and organization — both of which you are completely capable of.

What If Everything on My Report Is Accurate?

This is a question I want to address directly, because I think it trips people up.

If you review your credit report and everything on it is accurate — every late payment, every collection, every charge-off — you still have options. They're just different options.

Accurate negative information can sometimes be removed through goodwill letters (for isolated late payments with good history). Collection accounts can sometimes be resolved through pay-for-delete agreements. Bankruptcies and charge-offs will age off with time. And going forward, every on-time payment, every reduction in your utilization ratio, and every year that passes without new negative marks is actively improving your score.

Credit repair is not only about removing what's there. It's also about understanding what's there, making informed decisions about how to handle it, and building better habits going forward. Both matter.

Get the Complete Toolkit — Including the Credit Report Review Checklist

Reading your credit report carefully is step one of an organized credit repair process. Having the right tools to do it systematically makes all the difference.

Inside A Paralegal's Guide to Credit Repair, you'll find:

A complete credit report review checklist that walks you through every section of your Equifax, Experian, and TransUnion reports — field by field, account by account — so you never miss an error

160 pages of plain-English guidance covering credit reporting, consumer protection laws, dispute strategies, collector communication, and more

18 ready-to-use letter templates — dispute letters, goodwill letters, debt validation letters, follow-up letters, pay-for-delete letters, and more

A dispute tracker and certified mail log to keep every dispute organized from start to finish

A 30-day credit repair action plan so you always know your next step

Available for instant download at paralegalguides.com — at a launch price of just $17.

The Bottom Line

Your credit report is not a verdict. It is a document — and like any document, it can contain errors, outdated information, and items worth challenging.

But you can only challenge what you understand. And now you understand it.

Pull your reports. Go section by section. Use a checklist. Document what you find. Then take action — one letter, one account, one bureau at a time.

The process is more manageable than it looks from the outside. And you are more capable of navigating it than you've been led to believe.

→ Download the Credit Report Review Checklist + Full Toolkit for $17 at paralegalguides.com

Disclaimer: This post is for educational and informational purposes only. It does not constitute legal advice, financial advice, or credit counseling. Every situation is unique. Please consult a qualified attorney or financial professional for guidance specific to your circumstances.

Did this help you see your credit report differently? Share it with someone who's been putting off pulling theirs. Questions? Leave them in the comments — I answer every one.

xo A Paralegal's Guide to Credit Repair

Address

Alexandria Virginia 22304

United States of America

Contact

paralegalguides100@gmail.com

Subscribe to our newsletter

Paralegal Guides ™

Disclaimer: This website and product are for educational and informational purposes only. Nothing on this page is legal advice, financial advice, credit counseling, or a guarantee of any credit outcome. This product does not promise to remove accurate information from credit reports or guarantee credit score increases. Consumers should review their own circumstances and consult a qualified professional when needed.

© 2026. Paralegal Guides ™ | A Paralegals Guide to Credit Repair ™All rights reserved. Storks Enterprise LLC Privacy Policy | Cookie Policy

Social Media

Paralegal Guides

Plain-English, do-it-yourself legal guides and templates. By Charles, a working paralegal.