Goodwill Letter to Remove Late Payments

A goodwill letter to remove late payments from your credit report — even accurate ones. Get a free template, learn what to say, and find out what actually improves your odds.

5/25/202610 min read

Goodwill Letter to Remove Late Payments: Free Template + Step-by-Step Guide

By A Paralegal's Guide to Credit Repair | paralegalguides.com

Can I be honest with you for a second?

Late payments happen to good people. Really good people. People who lost a job, went through a divorce, had a medical emergency, or just had one genuinely overwhelming month where something slipped through the cracks. Life is not a perfectly organized spreadsheet, and sometimes a bill gets missed.

The problem is that your credit report doesn't know your story. It just sees a 30-day late. A 60-day late. A 90-day late. And it holds onto that information for up to seven years.

Seven years is a long time to pay for a mistake — especially when you've since paid the account, rebuilt your habits, and moved on.

Here's what most people don't know: you can ask a creditor to remove a late payment as an act of goodwill. There's no federal law that requires them to do it. But it happens — regularly — when you ask the right way, at the right time, with the right letter.

That letter has a name. It's called a goodwill letter. And in this post, I'm going to show you exactly how to write one, give you a free template you can use today, and walk you through the strategy that gives you the best shot at actually getting a yes.

Let's get into it.

What Is a Goodwill Letter?

A goodwill letter is a written request to a creditor — usually a credit card company, lender, or bank — asking them to remove a late payment from your credit report as an act of goodwill.

Unlike a credit dispute (which challenges information you believe is inaccurate), a goodwill letter acknowledges that the late payment happened. You're not saying it's wrong. You're asking the creditor to show some grace and remove it anyway, given your overall history with them and the circumstances around the missed payment.

This distinction is important. If the late payment is actually inaccurate — meaning it was reported in error, you have proof you paid on time, or the date is wrong — that's a dispute situation, not a goodwill letter situation. Disputes go to the credit bureaus. Goodwill letters go directly to the creditor.

But if the payment was genuinely late, a goodwill letter is your most direct path to getting it removed.

Does It Actually Work?

Yes — but let's be realistic about what "work" means here.

Creditors are not required to remove accurate late payments. The Fair Credit Reporting Act actually allows them to report accurate negative information for up to seven years. So when you send a goodwill letter, you are asking for a favor. You are appealing to a human being (or a team of human beings) to exercise discretion.

That means results vary. A lot.

Some creditors — especially those you've had a long, positive relationship with — will honor the request, particularly if the late payment was isolated and you've been on time ever since. Other creditors have stricter policies and may decline regardless of your circumstances. Some will say no the first time and yes the second. Some will never budge.

The factors that tend to improve your odds:

The late payment was a one-time occurrence, not a pattern

The account is now paid in full or in good standing

You've had a long relationship with the creditor (years of on-time payments)

You have a clear, genuine reason for why the payment was late

Your letter is professional, specific, and respectful — not entitled or demanding

You follow up more than once if you don't hear back

Is it guaranteed? No. Is it worth trying? Absolutely — especially because it costs you nothing but a stamp and a little time.

What to Include in Your Goodwill Letter

Before I give you the template, let's talk about what actually makes a goodwill letter effective. Because a generic, copy-paste letter that reads like a form submission is far less likely to get a response than something that feels personal and genuine.

1. A clear, specific explanation of what happened.

Not a saga, not a list of every hardship you've ever faced — just a concise, honest account of why the payment was late. Job loss. Medical issue. Family emergency. A one-time oversight during a move. Whatever is true. Creditors respond better to specificity than vague appeals.

2. Acknowledgment that the late payment occurred.

Don't try to deny it or imply it was their error if it wasn't. Own it. This actually builds trust rather than undermining it. It shows you're not trying to game the system — you're making a genuine request.

3. Evidence of your positive history.

If you've been a customer for five years and this is the only late payment on the account, say so. If you've been consistently on time before and since, point that out. You want them to see this late payment as the exception, not the pattern.

4. The specific action you're requesting.

Be direct. Ask them to remove the late payment notation from your credit report as reported to the major credit bureaus. Don't hint at it. State it clearly.

5. A professional, grateful tone.

You are asking for a favor. Even if you're frustrated by the situation, your letter needs to sound gracious, not entitled. Creditors are far more likely to say yes to someone who treats them with respect than someone who sounds like they're demanding special treatment.

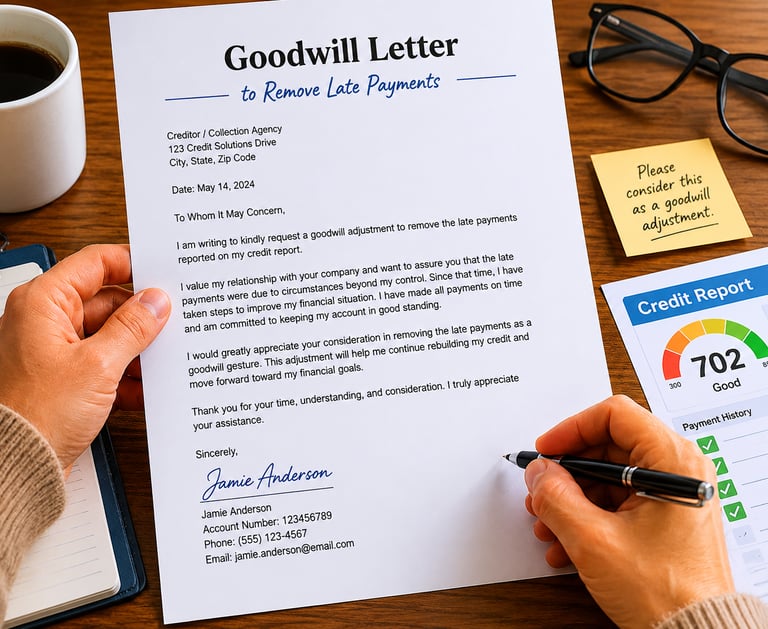

Free Goodwill Letter Template

Here's your template. Fill in the bracketed sections and adapt the language to match your specific situation. The more personal and specific you can make it, the better.

[Your Full Name] [Your Address] [City, State, ZIP] [Date]

[Creditor Name] [Creditor Address] [City, State, ZIP]

Re: Goodwill Adjustment Request — Account Number [Account Number]

Dear [Creditor Name] Customer Relations Team,

My name is [Your Name], and I have been a customer of [Creditor Name] since [Year]. I am writing to respectfully request a goodwill adjustment to my account history.

Specifically, I am requesting that you consider removing the [30/60/90]-day late payment notation from [Month, Year] as reported to the major credit bureaus — Equifax, Experian, and TransUnion.

I want to be transparent: the late payment did occur. At the time, I was experiencing [brief description of circumstances — e.g., an unexpected job loss / a medical emergency / a family crisis] that temporarily affected my ability to manage my finances. This was not a reflection of my typical financial behavior, and I take full responsibility for the missed payment.

Since that time, I have [brought the account current / maintained a consistent on-time payment record / paid off the balance in full]. I genuinely value my relationship with [Creditor Name] and have worked hard to get back on track.

I understand that you are not obligated to make this adjustment, and I am not suggesting that the information was reported in error. I am simply asking whether you might consider this a one-time exception given my overall account history and the circumstances involved.

This late payment is having a meaningful impact on my credit profile, and its removal would make a significant difference as I work toward [briefly mention goal — e.g., qualifying for a mortgage / securing an auto loan / rebuilding my overall credit health].

I am deeply grateful for your time and consideration. Please feel free to contact me at [Phone Number] or [Email Address] if you have any questions.

Respectfully,

[Your Signature] [Your Printed Name] [Account Number]

Take a moment to personalize this before you send it. The template gives you the structure — your story makes it compelling.

How to Send Your Goodwill Letter (And What to Do Next)

Step 1: Find the right address.

Don't send your goodwill letter to the general customer service address. Look for the creditor's credit disputes department or customer relations team address. This is usually on the back of your statement or on the creditor's website. Sending it to the right department gets it in front of the people who can actually act on it.

Step 2: Send it via certified mail.

Just like with a debt validation letter, you want a paper trail. Certified mail with return receipt gives you proof of delivery — and it signals that you're taking this seriously.

Step 3: Follow up.

This is the step most people skip — and it's often the difference between a no and a yes. If you don't hear back within 30 days, send a second letter. Be polite, reference your first letter and the date you sent it, and reiterate your request. Some creditors take two or three contacts before someone with authority actually reviews the account.

Step 4: Try a different channel if letters aren't working.

Some people have success calling the creditor's customer retention or executive resolution departments directly. If you go this route, have your account number ready, keep your tone calm and professional, and ask to speak with someone who has the authority to make goodwill adjustments. Follow up any verbal conversation with a written note confirming what was discussed.

Step 5: Log everything.

Write down the date you sent each letter, who you spoke to on the phone (if applicable), and what response you received. This keeps you organized and ensures you don't miss follow-up deadlines. A simple dispute tracker — like the one included in the A Paralegal's Guide to Credit Repair toolkit — makes this easy.

What About a Goodwill Letter Template for Multiple Late Payments?

This comes up a lot. What if you have more than one late payment on an account, or late payments across multiple accounts?

The honest answer: goodwill letters become less effective the more late payments there are, because it gets harder to frame a pattern as an isolated exception. That said, here's how to approach it strategically.

Prioritize by impact. A 90-day late payment hurts your credit score significantly more than a 30-day late. If you have to choose where to start, go after the most damaging ones first.

Send separate letters for separate accounts. Don't lump multiple creditors into one letter. Each creditor needs its own, personalized request. A letter addressed to "Creditor A" that also mentions "Creditor B" signals a mass campaign — and is far less likely to succeed.

Focus on recency. Late payments from the last two to three years have more impact on your credit score than older ones. As negative items age, their influence on your score diminishes naturally. If a late payment is six years old, it may make more sense to let it age off on its own than to spend energy requesting its removal.

If there's a genuine ongoing hardship, some creditors have formal hardship programs that go beyond goodwill adjustments — including temporary forbearance, reduced interest rates, or restructured payment plans. It may be worth asking about those options at the same time.

Goodwill Letters vs. Credit Disputes: Know the Difference

I mentioned this earlier, but it's worth spending a moment on because confusing these two processes can actually hurt your efforts.

A credit dispute is filed when information on your credit report is inaccurate, incomplete, or unverifiable. You file it with the credit bureaus — Equifax, Experian, TransUnion — under the Fair Credit Reporting Act. The bureau is required to investigate and respond within 30 days. If the information can't be verified, it must be removed.

A goodwill letter is sent directly to the creditor when the information is accurate but you're asking for it to be removed anyway. There's no legal obligation on the creditor's part. It's a request, not a demand.

Here's where it gets tricky: some people file a dispute hoping that the creditor won't respond to the bureau's investigation, causing the item to be removed by default. This is sometimes called a "frivolous dispute," and while it occasionally works, it can also backfire — bureaus may flag the dispute as unverifiable rather than removing it, and creditors are getting better at responding to verification requests. More importantly, if the information is accurate, filing a dispute stating otherwise isn't honest — and it's not a strategy I'd recommend building your credit repair process around.

The cleaner path: use disputes for genuine errors, and use goodwill letters for accurate late payments you're asking to have reconsidered. Know your tools. Use them correctly.

A Word on Patience — Because This Takes Longer Than You Think

I want to be upfront with you about something, because I think a lot of the credit repair content out there sets unrealistic expectations.

Removing late payments through goodwill letters is not a quick fix. It takes time to write the letters, wait for responses, follow up, and sometimes try again after a decline. The process can take weeks or months, especially if you're working across multiple accounts.

That is completely normal.

The people who see the best results from goodwill letters are the ones who approach the process with patience, organization, and persistence — not the ones who send one letter, get a no, and give up. If the first letter doesn't work, revise it, try a different contact at the company, or try a different channel.

Your credit history is worth the effort. A few negative marks that are removed can meaningfully shift your credit score — which affects the interest rate on your mortgage, whether you qualify for an apartment, the cost of your auto loan, and sometimes even whether you get the job you're applying for. That is real money over the course of your life.

Take it one step at a time. Stay organized. Keep going.

Want the Complete Credit Repair Toolkit?

If you're working through this process and want everything in one place — all the letters, all the trackers, and a complete roadmap from start to finish — I put it all together in A Paralegal's Guide to Credit Repair.

Here's what's inside:

160 pages of plain-English guidance on credit reports, consumer protection laws, dispute strategies, debt collector communication, goodwill letters, settlements, and more

18 ready-to-use letter templates — including goodwill letters, credit bureau dispute letters, debt validation letters, follow-up letters, and pay-for-delete request letters

A credit report review checklist to help you systematically identify what to dispute before you write a single letter

A dispute tracker and certified mail log so every date, every number, and every response is documented

A 30-day credit repair action plan so you always know exactly what to do next

It's available for instant download at paralegalguides.com — currently at a launch price of just $17.

The Bottom Line

A goodwill letter is one of the simplest, most underused tools in personal credit repair. It won't work every time. But it costs nothing to send, it requires no attorney, and for people who have an otherwise solid payment history with one unfortunate blip — it genuinely works.

Write it with honesty. Send it with documentation. Follow up with patience.

And remember: one late payment does not define your financial future. You're already doing the work to change the story — and that counts for more than you know.

→ Download the full Credit Repair Toolkit — including goodwill letter templates — for $17 at paralegalguides.com

Disclaimer: This post is for educational and informational purposes only. It does not constitute legal advice, financial advice, or credit counseling. Every situation is unique. Please consult a qualified attorney or financial professional for guidance specific to your circumstances.

Found this helpful? Share it with someone who's dealing with old late payments dragging down their score. And drop any questions in the comments — I'm here for it.

xo A Paralegal's Guide to Credit Repair

Address

Alexandria Virginia 22304

United States of America

Contact

contact@thedocpreparer.com

Subscribe to our newsletter

A Paralegal's Guide to Credit Repair ™

Disclaimer: This website and product are for educational and informational purposes only. Nothing on this page is legal advice, financial advice, credit counseling, or a guarantee of any credit outcome. This product does not promise to remove accurate information from credit reports or guarantee credit score increases. Consumers should review their own circumstances and consult a qualified professional when needed.

© 2026. A Paralegals Guide to Credit Repair ™All rights reserved. Storks Enterprise LLC Privacy Policy | Cookie Policy