Free Debt Validation Letter Template (And Exactly How to Use It)

Get a free debt validation letter template and learn exactly how to use it. Know your FDCPA rights, send it the right way, and stop debt collectors in their tracks.

Paralegal Guides

5/25/202611 min read

What is a Debt Validation Letter?

Free Debt Validation Letter Template (Word + PDF) | A Paralegal's Guide to Credit Repair

Let me guess.

You got a call — or maybe a letter — from a debt collector. Your stomach dropped. Maybe you recognized the debt, maybe you didn't. Either way, something felt off, and you weren't sure what you were actually supposed to do next.

So you did what most of us do. You Googled it. You found terms like "FDCPA" and "validation of debt" and "cease and desist," and now your head is spinning even more than it was before.

Here's what I want you to know right now, before we go any further: you have more power in this situation than you think. Federal consumer protection laws give you the right to request written proof that a debt collector has the right to collect from you — before you pay a single cent. And the tool you use to exercise that right is called a debt validation letter.

In this post, I'm going to give you a free debt validation letter template you can use today, walk you through exactly how it works, explain what happens after you send it, and help you avoid the mistakes that can accidentally make things worse.

Let's dive in.

Before we get to the template, let's make sure we're on the same page about what this letter actually does — because there's a lot of confusion out there.

A debt validation letter (also called a debt verification letter) is a written request you send to a debt collector asking them to prove that:

The debt is actually yours

The amount they're claiming is accurate

They have the legal right to collect it from you

This matters more than most people realize. Debt gets bought and sold constantly. An original creditor — say, a credit card company — will often sell delinquent accounts to a third-party debt collection agency for pennies on the dollar. That agency may then sell it to another collector. By the time someone is calling you, the paper trail can be a mess. Amounts get inflated. Accounts get misassigned. People get contacted for debts that aren't even theirs, debts that are past the statute of limitations, or debts that have already been paid.

Your debt validation letter puts the collector on notice that you know your rights — and that you're not going to pay blindly.

Here's the key legal foundation: the Fair Debt Collection Practices Act (FDCPA) is a federal law that governs how third-party debt collectors are allowed to behave. Under the FDCPA, you generally have the right to request validation of a debt in writing. When you exercise that right, collectors are typically required to stop collection activity until they provide the requested verification.

That said — and this is important — this guide is for educational purposes only. It is not legal advice. Every situation is different, and if you're dealing with a lawsuit, a garnishment threat, or significant amounts of money, please consult a qualified attorney. What I can do is help you understand the process so you can move forward with more confidence and clarity.

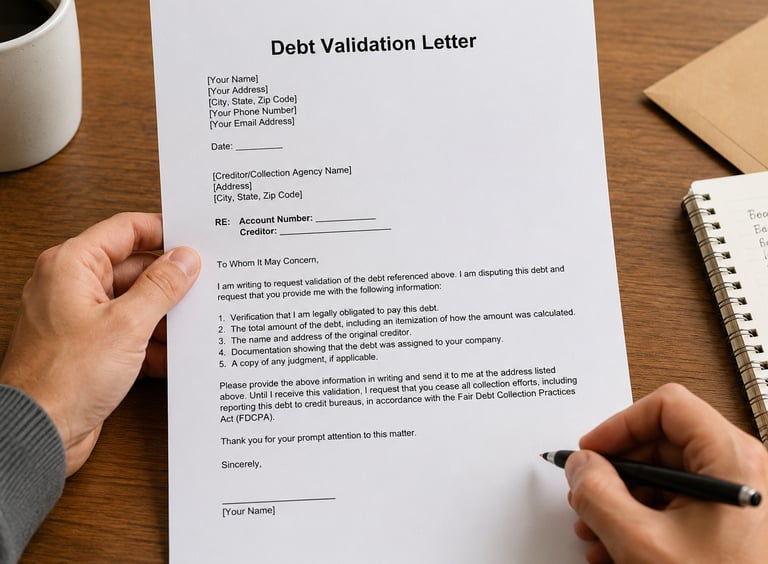

The Free Debt Validation Letter Template

Here it is. Copy this, fill in the bracketed sections with your information, and send it via certified mail with return receipt requested (more on why that matters in a moment).

[Your Full Name]

[Your Address]

[City, State, ZIP]

[Date]

[Debt Collector Company Name] [Debt Collector Address] [City, State, ZIP]

Re: Account Number [Account Number, if known] — Request for Debt Validation

Dear Sir or Madam,

I am writing in response to your [letter / phone call] dated [Date], regarding the alleged debt referenced above. I am requesting that you provide written verification of this debt as permitted under the Fair Debt Collection Practices Act, 15 U.S.C. § 1692g.

Please provide the following:

The name and address of the original creditor

The amount of the debt, including an itemized breakdown of any fees, interest, or penalties added to the original balance

Proof that your company is licensed to collect debts in [Your State]

A copy of the original signed agreement or contract that created this alleged debt

Verification that the statute of limitations has not expired on this account

The name and address of the original creditor if different from the current collector

Until this debt is verified in writing and returned to me, please cease all collection activity, including phone calls, letters, and credit reporting, as required by law.

Please note that I am keeping records of all communications related to this matter, including dates, times, and content of any contact.

Sincerely,

[Your Signature] [Your Printed Name]

Feel free to save this, print it, or adapt it to your situation. And if you want a professionally formatted, print-ready version along with 17 other dispute and collector response templates, you can grab the full toolkit at paralegalguides.com — but more on that in a moment.

How to Send Your Debt Validation Letter (This Part Really Matters)

Writing the letter is just step one. How you send it determines whether it actually protects you.

Step 1: Send it via certified mail with return receipt requested.

I cannot stress this enough. Do not email it. Do not fax it. Do not hand-deliver it without documentation. Certified mail through the USPS gives you a tracking number and — when you add the return receipt — a green card that comes back to you with the collector's signature proving they received it. That paper trail is your protection if they claim they never got your request.

Step 2: Keep a copy of everything.

Make a copy of your letter before you send it. Keep the tracking number. When the green return receipt card comes back, staple it to your copy of the letter and put it somewhere safe. If you have a Dispute Tracker (there's one included in the full guide), log the date sent, the certified mail number, and the response deadline.

Step 3: Know your timing.

If you received the initial collection notice within the last 30 days, you're within the standard FDCPA window and your rights are clear. If it's been longer, the rules may be different — which is one reason it's worth understanding the law before you act, not after.

Step 4: Wait. Don't pay anything yet.

Once you've sent your validation letter, wait for their response before taking any action. Paying the debt before receiving validation — or worse, before confirming that the debt is actually yours and the amount is accurate — can sometimes complicate your situation.

What Happens After You Send It?

This is where most people get anxious, so let's talk through the realistic scenarios.

Scenario 1: The collector responds with proper verification.

If the collector responds with documentation — the original creditor's name, the account history, proof of the amount owed — then you have something to review. This doesn't automatically mean you owe the money. It means you now have information to work with. From here, you might review the documents carefully, check the statute of limitations in your state, and decide whether to dispute the amount, negotiate a settlement, or request a pay-for-delete agreement.

Scenario 2: The collector ignores your letter or can't verify the debt.

This happens more often than you'd expect. If a collector can't validate the debt, they are generally required to cease collection efforts. If they continue to call or contact you anyway, that may be a violation of the FDCPA — and violations can have consequences for collectors. Keeping your documentation (see Step 2 above) is what makes this actionable.

Scenario 3: The collector sells the debt to someone else.

Unfortunately, even if one collector backs off, the debt can be sold to a new collector who starts the process over. The same rules apply — you can send a new validation letter to the new collector. Yes, it can feel exhausting. That's exactly why staying organized matters so much.

Scenario 4: You're taken to court.

If the debt is large and the collector has documentation, they may pursue legal action. If that happens, please consult an attorney. A debt validation letter is not a magic eraser — it's a tool for exercising your rights and getting organized. Know the difference.

The Mistakes That Can Undermine Your Efforts

Okay, let's talk about what NOT to do — because I see people make these mistakes all the time, and they can genuinely hurt your position.

Mistake #1: Sending an emotional or vague letter.

I get it. If a debt collector has been aggressive or calling at all hours, you're frustrated. But sending an angry, scattered letter is not going to help you. Your letter needs to be calm, professional, and specific. The template above is a good example of the right tone.

Mistake #2: Calling instead of writing.

Phone calls are not documented. Even if you have a conversation where the collector says they'll "look into it," you have nothing in writing. Always put your request in writing, always send it certified mail, always keep the receipt.

Mistake #3: Ignoring a debt hoping it will go away.

Silence is not a strategy. Debt doesn't disappear because you don't respond — it can grow, get sold, and eventually impact your credit report or result in legal action. Even if you're not sure the debt is yours, engaging through the proper process (like sending a validation letter) is almost always better than hoping for the best.

Mistake #4: Making a payment before validating.

Making a payment — even a small one — can sometimes restart the statute of limitations on a debt in certain states. Before you pay anything, make sure you understand what you're dealing with. Validate first. Understand the timeline. Then decide.

Mistake #5: Not tracking your responses.

The FDCPA has specific timelines. If you don't know when you sent your letter or when you received a response, you lose the ability to enforce your rights effectively. Use a tracker. Write it down. Treat this like the legal process it is, because it is one.

What About Your Credit Report?

Great question — and one that often gets confused with the validation process.

Sending a debt validation letter to a collector is not the same thing as disputing an item on your credit report. These are two separate processes handled by two different parties.

If the debt appears on your credit report and you believe it's inaccurate, outdated, or doesn't belong to you, you can dispute it directly with the credit bureaus — Equifax, Experian, and TransUnion — under the Fair Credit Reporting Act (FCRA). You have the right to dispute inaccurate information, and the bureaus are generally required to investigate and respond.

The debt validation letter goes to the collector. The credit report dispute goes to the bureau. In some situations, you may want to do both — but understanding which letter goes where is essential to getting the outcome you're after.

If you want a step-by-step walkthrough of both processes — including sample credit bureau dispute letters alongside collector response templates — that's exactly what A Paralegal's Guide to Credit Repair covers. More on that below.

You Deserve to Understand This Process

Here's something I want to say out loud, because I think it needs to be said:

The credit and debt collection system is complicated by design. The legal language is dense. The timelines are specific. The letters feel intimidating. And collectors know that most consumers won't push back because they don't know their rights.

But you're here. You're reading this. You're doing the work to understand what's actually going on — and that already puts you ahead of most people in your situation.

You don't need to be a lawyer to take organized, informed action on your own credit. You need a clear process, the right templates, and enough understanding of the rules to know when you're being protected and when you need to escalate.

That's exactly what this guide exists to give you.

Ready to Go Deeper? Here's What's Inside the Full Toolkit.

The free template above is a solid starting point — but credit repair is rarely a one-letter process. Between disputing credit bureau errors, responding to collector communications, writing goodwill letters to remove late payments, and tracking every certified mail number and response deadline, there's a lot to manage.

That's why I created A Paralegal's Guide to Credit Repair — a 160-page PDF guide designed specifically for everyday consumers who want to understand the system and take organized, confident action.

Here's what's included:

The full 160-page guide covering credit reports, consumer protection laws (FCRA, FDCPA, CROA), dispute strategies, debt collector communication, settlements, goodwill letters, and more — in plain English

18 ready-to-use letter templates including credit bureau dispute letters, debt validation letters, follow-up letters, goodwill letters, and pay-for-delete request letters

A credit report review checklist to help you systematically identify errors before you dispute

A dispute tracker and certified mail log so you never lose track of what you sent, when, and what happened next

A 30-day credit repair action plan to help you move through the process step by step instead of feeling overwhelmed

The entire toolkit is available for instant download at paralegalguides.com — currently at a launch price of just $17.

Frequently Asked Questions About Debt Validation Letters

Can I send a debt validation letter for an old debt?

Yes — but timing matters. The FDCPA gives you the clearest protections when you send your validation request within 30 days of receiving the first written notice from a collector. After that window, the collector isn't legally required to stop collection activity while they verify the debt, though they still can't make false claims about it. That said, there are other protections that may still apply to older debts, including statutes of limitations that vary by state and debt type. When in doubt, research the statute of limitations in your state before taking action on older accounts.

Does sending a debt validation letter hurt my credit?

No. Sending a letter to a debt collector has no direct impact on your credit report. What shows up on your credit report is the account itself — which was already there before you sent the letter. The letter is a private communication between you and the collector.

What if the debt is from a debt I actually owe?

Sending a validation letter doesn't mean you're denying you owe the debt. It means you want the collector to prove the amount is accurate, the account is yours, and they have the legal right to collect it. Even if you know you owe a debt, verifying the details before paying is a smart move — amounts can be inflated, accounts can be mishandled, and knowing the original creditor's information helps you make better decisions about how to resolve it.

Can a debt collector sue me after I send a validation letter?

Yes. A debt validation letter is not a lawsuit shield. If a collector has documentation and the debt is within the legal statute of limitations, they can still pursue legal action. If you receive notice of a lawsuit, respond — ignoring it can result in a default judgment against you. In that situation, speaking with an attorney is the wisest next step.

Can I use this template for medical debt?

The FDCPA covers third-party debt collectors, which includes many medical debt collectors. If a collection agency is contacting you about a medical bill (rather than the original hospital or provider), this letter can apply. However, medical debt has some unique rules, including specific credit reporting changes in recent years. Be sure to verify the current rules for your situation.

The Bottom Line

A debt validation letter is one of the most powerful tools available to consumers dealing with debt collectors — and it costs nothing to send. It puts you in the driver's seat. It forces the collector to prove what they're claiming. And it creates a paper trail that protects you if things escalate.

The key is to send it the right way (certified mail), at the right time (as soon as possible after first contact), with the right language (professional, specific, and documented).

You've already taken the first step by doing your research. Now take the next one.

→ Download the full Credit Repair Toolkit for $17 at paralegalguides.com

Disclaimer: This post is for educational and informational purposes only. It does not constitute legal advice, financial advice, or credit counseling. Every situation is unique. Please consult a qualified attorney or financial professional for guidance specific to your circumstances.

Did this help you? Share it with someone who's dealing with debt collectors and doesn't know where to start. And if you have questions, drop them in the comments — I read every single one.

xo A Paralegal's Guide to Credit Repair

Address

Alexandria Virginia 22304

United States of America

Contact

paralegalguides100@gmail.com

Subscribe to our newsletter

Paralegal Guides ™

Disclaimer: This website and product are for educational and informational purposes only. Nothing on this page is legal advice, financial advice, credit counseling, or a guarantee of any credit outcome. This product does not promise to remove accurate information from credit reports or guarantee credit score increases. Consumers should review their own circumstances and consult a qualified professional when needed.

© 2026. Paralegal Guides ™ | A Paralegals Guide to Credit Repair ™All rights reserved. Storks Enterprise LLC Privacy Policy | Cookie Policy

Social Media

Paralegal Guides

Plain-English, do-it-yourself legal guides and templates. By Charles, a working paralegal.