Credit Repair Letters PDF

Get the complete guide to credit repair dispute letters — what to write, who to send them to, and how to track results. Includes free templates for every stage of the process.

5/25/202611 min read

Credit Repair Letters PDF: The Complete Dispute Letter Guide

By A Paralegal's Guide to Credit Repair | paralegalguides.com

Here's something nobody tells you when you first start researching credit repair.

It's not one letter. It's not one process. It's not one bureau, one creditor, or one phone call that fixes everything.

Credit repair — real, organized, effective credit repair — is a series of written communications, sent to the right people, in the right order, documented carefully along the way. And the tool that makes all of it possible is something most people have never heard of until they're already deep in the weeds:

A credit repair dispute letter.

If you've been searching for credit repair letters in PDF format, chances are you already sense that writing is the right approach. You're right. Written letters create paper trails. Paper trails create accountability. And accountability is exactly what the credit reporting system — which is full of errors, outdated information, and misassigned accounts — needs someone to demand.

In this guide, I'm going to walk you through every type of credit repair letter you might need, who each one goes to, when to use it, and what it should say. This is the complete picture — not just one letter for one situation, but the full toolkit for anyone who wants to take a serious, organized run at cleaning up their credit report.

Let's do this.

First, Understand Who You're Writing To

One of the biggest sources of confusion in credit repair is figuring out who actually receives each letter. Before we get into the templates, let's get crystal clear on the three parties involved — because sending the wrong letter to the wrong party is one of the most common and costly mistakes people make.

The Credit Bureaus Equifax, Experian, and TransUnion are the three major credit reporting agencies. They collect information from creditors and compile it into your credit report. When you believe information on your credit report is inaccurate, outdated, or unverifiable, you dispute it directly with the bureau reporting it. The bureau then has 30 days to investigate and respond.

The Original Creditors These are the banks, credit card companies, lenders, and service providers that originally extended you credit. If you have a late payment, a charge-off, or an account you want handled a specific way, you often need to communicate directly with the original creditor — not the bureau. Goodwill letters, pay-for-delete requests, and account verification requests sometimes go here.

Debt Collectors Third-party collection agencies that purchase or are assigned delinquent debts. Debt validation letters go to collectors. Cease and desist letters go to collectors. These are separate from the bureaus and often separate from the original creditor.

Why this matters: A dispute sent to the wrong party will either be ignored or bounced back to you with no action taken. Knowing exactly who receives each letter — and why — is the foundation of an effective credit repair strategy.

The 7 Credit Repair Letters You Need to Know

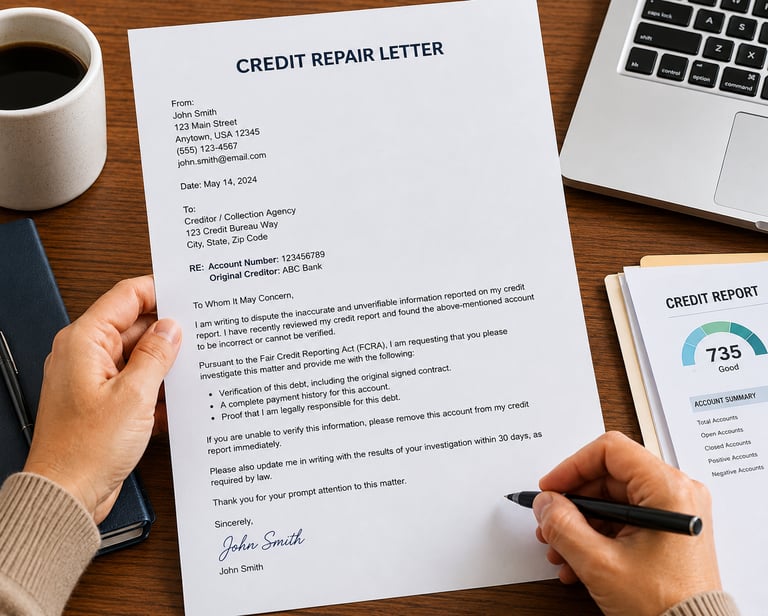

Letter #1: The Credit Bureau Dispute Letter

Who it goes to: Equifax, Experian, and/or TransUnion When to use it: When you find inaccurate, outdated, incomplete, or unverifiable information on your credit report

This is the foundational credit repair letter — the one most people think of when they imagine "disputing" something on their credit report. Under the Fair Credit Reporting Act (FCRA), you have the right to dispute any information on your credit report that you believe is inaccurate or cannot be verified. The bureau must investigate and respond within 30 days (or 45 days in some circumstances).

What to include:

Your full name, address, date of birth, and the last four digits of your Social Security number (for identity verification)

A clear description of each item you are disputing, including the account name, account number, and the specific reason for the dispute

A request that the bureau investigate and remove or correct the item if it cannot be verified

Copies (not originals) of any supporting documentation — statements, payment records, identity documents

What to dispute:

Accounts that don't belong to you

Late payments you have proof were made on time

Incorrect balances or credit limits

Accounts that should have aged off (most negative items must be removed after seven years)

Duplicate accounts listed more than once

Incorrect personal information (wrong address, misspelled name, wrong Social Security number)

Pro tip: Dispute each item separately and clearly. A letter that disputes ten things at once in a vague, scattered way is far less effective than specific, itemized disputes with supporting evidence attached.

Letter #2: The Follow-Up Dispute Letter

Who it goes to: The credit bureau When to use it: When you don't receive a response within 30–45 days, or when the bureau's investigation result is unsatisfactory

The first dispute doesn't always get the result you're looking for. Sometimes bureaus respond that an item has been "verified" without providing any real detail about how they verified it. Sometimes they simply don't respond at all. That's when the follow-up dispute letter comes in.

What to include:

Reference to your original dispute, including the date it was sent and a copy of your certified mail receipt

A reiteration of the specific item being disputed and the reason

A request for the method of verification — you have the right to know how the bureau verified the information

A statement that if the item cannot be properly verified, it must be removed under the FCRA

This letter applies a little more pressure. It signals that you understand the process, you know your rights, and you're not going away. That matters.

Letter #3: The Debt Validation Letter

Who it goes to: The debt collector When to use it: When a collection agency contacts you about a debt and you want them to prove it's valid before you take any action

We covered this in depth in Article #1 of this series, so I won't repeat every detail here — but it belongs in this guide because it's a core piece of the credit repair letter toolkit.

The short version: under the Fair Debt Collection Practices Act (FDCPA), you have the right to request written verification of a debt. Until the collector validates the debt, they are generally required to stop collection activity. Send this letter via certified mail as soon as possible after first contact — ideally within 30 days of receiving the initial notice.

What to request:

The name and address of the original creditor

An itemized breakdown of the amount claimed

Proof that the collector has the legal right to collect the debt

Verification that the statute of limitations has not expired

Letter #4: The Goodwill Letter

Who it goes to: The original creditor When to use it: When a late payment is accurate but you want to ask the creditor to remove it as an act of goodwill

Also covered in detail in Article #2, but equally essential here. The goodwill letter is the tool for accurate negative information that you're asking a creditor to reconsider — not because they made an error, but because of your overall history, your circumstances at the time, and a genuine appeal to their discretion.

The key ingredients: honesty about what happened, evidence of your positive history with the creditor, a specific request for removal, and a respectful, professional tone. No entitlement. No anger. Just a genuine ask from someone who has clearly done the work to get back on track.

Letter #5: The Pay-for-Delete Letter

Who it goes to: The debt collector or original creditor When to use it: When you're willing to pay a collection account in exchange for the collector agreeing to remove it from your credit report

This is one of the most misunderstood letters in credit repair — and one of the most potentially powerful.

Here's how it works: a collection account on your credit report is damaging. But if you simply pay it without negotiating, it often remains on your report as a "paid collection" — which is still negative. A pay-for-delete agreement asks the collector to remove the account entirely from your credit report in exchange for payment.

Important caveats: Not all collectors will agree to this. Some have blanket policies against pay-for-delete arrangements. And while pay-for-delete is not explicitly illegal, the credit bureaus have historically discouraged it. In practice, results vary widely. Some collectors honor the agreement; others don't even after receiving payment. That's why you get the agreement in writing — always — before sending a single dollar.

What your pay-for-delete letter should request:

Written confirmation that upon receipt of your payment, the collector will request deletion of the account from all three credit bureaus

The specific amount being paid and the account it applies to

A deadline for their written response before you take action

Never pay first and ask for deletion later. Get the written agreement, keep a copy, then pay.

Letter #6: The Cease and Desist Letter

Who it goes to: The debt collector When to use it: When you want a collector to stop all contact with you entirely

Under the FDCPA, you have the right to tell a debt collector to stop contacting you. Once they receive a written cease and desist letter, they are generally only permitted to contact you one final time — to confirm they will stop, or to notify you of a specific action they intend to take (such as filing a lawsuit).

What this letter does NOT do: It does not make the debt go away. It does not prevent a collector from suing you. It does not remove the account from your credit report. It simply stops the phone calls, letters, and contact attempts.

This letter is most useful when a collector is contacting you repeatedly, at inconvenient times, or in ways that may violate the FDCPA — and you want the communication to stop while you figure out your next move. Use it strategically, not reflexively. Silence from a collector isn't always the goal — sometimes you need information from them first.

Letter #7: The Method of Verification Request

Who it goes to: The credit bureau When to use it: After a bureau responds that a disputed item has been "verified" and you want to know exactly how

This is a letter most people don't know exists — and it can be a game changer.

When a bureau investigates your dispute and tells you an item has been verified, they are not required to give you a detailed explanation of how they verified it. But you can ask. And asking — in writing, via certified mail — sometimes reveals that the "verification" was cursory or inadequate, which can open the door to a more successful second dispute or a different avenue of challenge.

What to request:

The name, address, and phone number of the person or entity that verified the disputed information

A description of the procedure used to determine the accuracy of the item

Any documentation used in the verification process

This letter is not guaranteed to produce results. But it is a legitimate tool, it puts the bureau on notice that you're paying attention, and it occasionally leads to removals that a standard dispute did not.

How to Send Every One of These Letters

The method of delivery matters just as much as the content. Here are the rules that apply across every letter in this toolkit:

Always send via certified mail with return receipt requested. This gives you proof of delivery — the green card that comes back with the recipient's signature. Without it, the other party can claim they never received your letter, and you have no recourse.

Always keep a copy. Before the letter leaves your hands, make a copy. Keep it with the certified mail receipt and the return receipt card in a dedicated folder — physical or digital — for each account you're working on.

Always date your letters. Timelines matter in this process. The FCRA gives bureaus 30 days to investigate. The FDCPA has its own windows. If you don't know when you sent something, you can't hold anyone accountable to a deadline.

Never send original documents. If you're attaching supporting evidence — payment records, statements, prior correspondence — always send copies. Keep the originals safe.

Track everything. Every letter sent, every certified mail number, every response received, every deadline. A dispute tracker is not optional if you're working on more than one item at a time. It is the thing that keeps you organized and keeps the process moving.

A Note on "609 Letters" and Credit Repair Myths

You've probably come across the term "609 letter" if you've spent any time researching credit repair online. The claim is that Section 609 of the Fair Credit Reporting Act gives you a special, powerful right to demand removal of negative items — and that a "609 letter" is a secret the credit industry doesn't want you to know about.

Here's the honest truth: Section 609 of the FCRA is simply the section that gives you the right to request your credit file disclosure. It doesn't contain a magic removal clause. There is no secret loophole. A "609 letter" is really just a dispute letter — the same letter we've already covered — dressed up in language that implies special legal power it doesn't actually have.

That doesn't mean dispute letters don't work. They absolutely do — when used correctly, for genuinely inaccurate or unverifiable information, sent to the right party, with proper documentation. That's the real strategy. Not a secret section number, but a clear, organized, documented process.

I want you to go into this with accurate expectations, because unrealistic expectations lead to shortcuts — and shortcuts lead to wasted time and money.

The Order of Operations

If you're staring at your credit report and feeling overwhelmed by everything that needs to happen, here's a simple sequence to follow:

Step 1: Pull all three credit reports (free at AnnualCreditReport.com) and review them carefully using a credit report review checklist.

Step 2: Identify every item that is inaccurate, outdated, unverifiable, or doesn't belong to you.

Step 3: For items being reported by the bureaus that you believe are wrong — send credit bureau dispute letters (Letter #1).

Step 4: For collection accounts — send debt validation letters (Letter #3) before paying anything.

Step 5: For accurate late payments with otherwise good history — send goodwill letters (Letter #4) directly to the creditor.

Step 6: For collection accounts you're ready to resolve — consider a pay-for-delete agreement (Letter #5) before paying.

Step 7: Follow up on everything. If a bureau doesn't respond or the result is unsatisfactory, send follow-up letters (Letter #2) and method of verification requests (Letter #7).

Step 8: If a collector continues contacting you inappropriately — send a cease and desist letter (Letter #6).

This is not a one-week process. It is a months-long, organized campaign. The people who see real results are the ones who stay consistent, stay documented, and don't give up after the first no.

Get All 7 Letters — Plus More — in One Place

Writing all of these letters from scratch takes time. Getting the language right — professional without being aggressive, specific without being wordy, legally grounded without being confusing — takes even more.

That's exactly why I created A Paralegal's Guide to Credit Repair.

Inside the toolkit you'll find:

160 pages of plain-English guidance on every stage of the credit repair process — from reading your reports to negotiating with collectors

18 ready-to-use letter templates covering every letter type in this guide, plus variations for different scenarios

A credit report review checklist so you never miss an error before you start writing

A dispute tracker and certified mail log to keep every account, every deadline, and every response organized in one place

A 30-day credit repair action plan so you always know your next move

Available for instant download at paralegalguides.com — at a launch price of just $17.

The Bottom Line

Credit repair letters are not magic. They don't erase accurate history overnight, and no single letter is a guaranteed fix. But used correctly — sent to the right people, at the right time, with proper documentation — they are among the most powerful tools available to everyday consumers who want to take organized, informed control of their credit.

You don't need to be an attorney. You don't need to pay a monthly credit repair service. You need the right letters, the right process, and the consistency to see it through.

You've already got the knowledge. Now you've got the toolkit.

→ Download the complete Credit Repair Letter Toolkit for $17 at paralegalguides.com

Disclaimer: This post is for educational and informational purposes only. It does not constitute legal advice, financial advice, or credit counseling. Every situation is unique. Please consult a qualified attorney or financial professional for guidance specific to your circumstances.

Was this helpful? Share it with someone who's been staring at their credit report not knowing where to start. Questions? Drop them in the comments.

xo A Paralegal's Guide to Credit Repair

Address

Alexandria Virginia 22304

United States of America

Contact

paralegalguides100@gmail.com

Subscribe to our newsletter

Paralegal Guides ™

Disclaimer: This website and product are for educational and informational purposes only. Nothing on this page is legal advice, financial advice, credit counseling, or a guarantee of any credit outcome. This product does not promise to remove accurate information from credit reports or guarantee credit score increases. Consumers should review their own circumstances and consult a qualified professional when needed.

© 2026. Paralegal Guides ™ | A Paralegals Guide to Credit Repair ™All rights reserved. Storks Enterprise LLC Privacy Policy | Cookie Policy

Social Media

Paralegal Guides

Plain-English, do-it-yourself legal guides and templates. By Charles, a working paralegal.